Home Country Bias – Diversification Part 1

I just recently read a couple of fascinating investing books and started listening to new podcasts that opened my mind to novel investing ideas that differ from the traditional dividend investing concept that has treated me so well this past decade. These ideas are fascinating because they appeal to the quantitative part of my brain.

I’m going to attempt to get some of these thoughts to paper by writing a multipart series discussing them. In short, they will be all based on the theme of diversification with an emphasis towards increasing performance as well as decreasing volatility. Yes, dividends will still be a part of them.

What investing books and podcasts peaked my interest? Stick around to find out. I don’t want to spoil the surprises by revealing my sources too soon.

Diversification Series:

Part 1: Home Country Bias

Part 2: Portfolio Realignment

Part 3: Alternative Investments

Home Country Bias

Do you have home country bias? What is home country bias, you ask? It is favoring companies in your own country over companies in other countries.

It is not unusual. Investors are much more likely to favor companies they are familiar with.

Consider a simple example of a slightly different scenario: Imagine the person that invests a disproportionate amount in his own company. There are very positive reasons why he chooses to do so. He understands the company better than most people and is very motivated to do well to continue to move the company (and its stock price) forward. He may even be able to invest in the company at a discount. These all seem like very valid reasons to invest in the company you work for.

Why could this be bad? Let’s say the company starts struggling or even goes bankrupt. In both situations that person could be laid off and then, in addition to not having a job, he would then lose much or all of the money he invested. Think of an Enron situation for the worst case scenario. Some of those employees that were too heavily invested were out of a job and lost the majority of their retirement savings.

By diversifying to investments outside of the company you work for or even outside the same industry, you reduce the risk of such an event happening.

A similar concept can be applied to the broader idea of investing in the country in which you live.

According to JP Morgan, the US is 52% of the world. For a US investor then, having more than 52% invested in US stocks would be considered home country bias.

As an American, I do tend to think of the United States as being exceptional. Maybe it does deserve a higher percentage than its world weighting would suggest? After all, US companies are some of the most innovative and successful in the world. That seems true for the majority of the 20th century. Will it continue for the 21st? Who knows!?

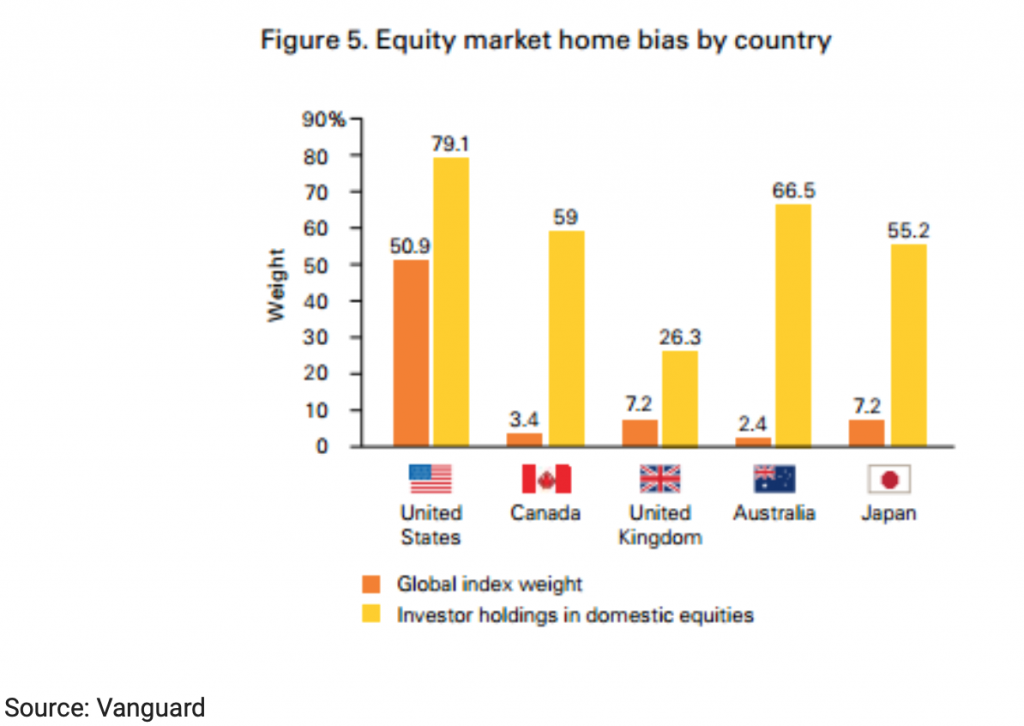

It is not just the US that has home country bias

Surprisingly, it is not just US investors that feel that their country is special.

Looking at the chart above you’ll notice that the citizens of some countries are even more heavily skewed to a home country bias than the average US investor. This largely stems from the fact that the US is such a large component of the global weighting that a higher percentage allocated to it is appropriate.

When I think about the stocks in my own portfolio, I know I “suffer” from a home country bias as well. (Fortunately, for the last decade or so this bias as served me very well!)

My own home country bias

I just did the calculations and when I count all equities, including taxable brokerage accounts, Roth IRA, and 401(k), 89% of my portfolio is invested in US equities. Of the 11% that is invested in foreign companies, 88% of those companies are traded on US exchanges as ADRs or on the pink sheets (for Nestle). The other 12% of my foreign investments is traded via a Schwab Global Account and is denominated in foreign currencies (Canadian dollars at the moment).

So, thus far in my account I am making an active bet that the US will continue to outperform the rest of the world.

Yes, an active bet.

You would think that investing in ETFs that track S&P 500 or the Vanguard Total Stock Market Index (VTSMX) would be the definition of passive investing. However, even these ETFs are making an active bet in the US over that of other countries.

For those of us that enjoy steady stock growth with solid dividend increases, sticking with US companies may be okay. The US may not be the best performer for the 21st century, but it definitely won’t be the worst performer either. In fact, most successful US companies (many of the ones that we are all invested in), are also very successful overseas. Apple, for example, recently noted in its 2019 fiscal fourth quarter, that international sales accounted for 60% of the quarter’s revenue. We are getting quite a bit of international exposure by simply investing in US stocks.

What is important, dividends or total portfolio value?

When I sat back and thought about what I am actually interested in doing with my portfolio, I learned that I am interested in total gains, which includes contributions from dividends, buy backs, and capital gains, rather than just seeing the 12-month forward dividend number increase. The ultimate goal is to increase portfolio value as quickly as possible. I am in my earning years and do not rely on dividend income to survive.

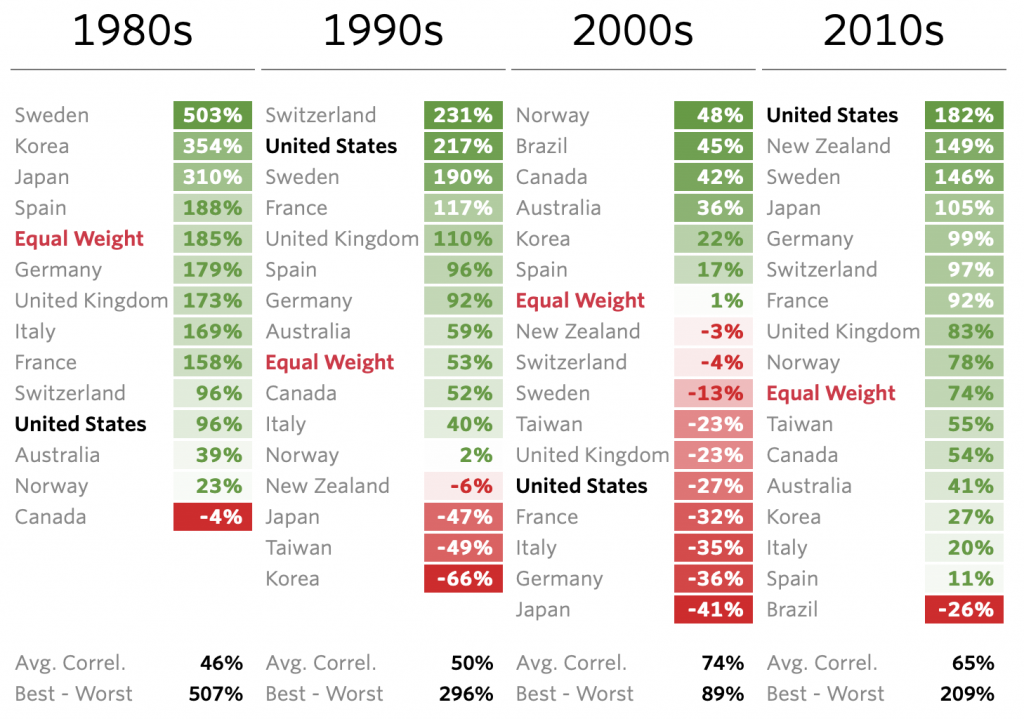

Take a look at the next chart.

United States is not always the best performer

The United States was a weak performer in the 1980s, one of the strongest performers in the 1990s, one of the worst performers in the 2000s, and the top performer so far in the 2010s. By choosing to stay invested in just dividend stocks and just in the United States, for instance, you are making an active bet in two things. One, that dividend paying stocks will outperform “value” or “growth.” And, two, that the United States is the best place to be invested. As shown by the chart above, this is not always the case.

If you follow the link above you will see that since the 1900s, the United States has only been the best performer in the 1900s, 1910s, and 2010s. Now, most of those other decades, the US wasn’t the worst performer and was only negative in the 1930s (-12%), 1970s (-17%), and 2000s (-27%). Obviously, a buy-and-hold approach investing only in the US since the 1900s would have done incredibly well. But, there is an opportunity cost of not diversifying into foreign markets…you would have missed out on even more extraordinary gains.

Upcoming Part 2 of the Diversification Series

In Part 2 of this series I will be discussing how I am realigning by portfolio to help account for this bias and theories on the best ways to do that.

Sources:

1a) The Biggest Valuation Spread in 40 Years?

1b) Podcast Episode #175: The Biggest Valuation Spread In 40 Years?

2) Geographic Diversification Can Be a Lifesaver, Yet Most Portfolios Are Highly Geographically Concentrated

Hahaha this is so true! People are so home focused when making portfolio decisions. Investing in one’s own company, as an employee, is also a big risk factor for many – also a kind of home bias. Exposes one for very high overall correlation and low diversification.

TradingGator recently posted…How to Start Trading Plus500 Bitcoin CFDs?

Hi TradingGator,

Thanks for commenting. It has been fun writing up this diversification series. It has definitely affected how I am allocating my own funds.

Scott

So true!!!!

Living in Canada, were only 3% of the global mkt, yet most investors don’t have a single penny outside our border!!

I’ve invested nearly 100% of my savings in recent years to investments in the US. It’s tough to find investment in Europe!!

Country style will perfectly suit you, if you prefer a comfortable, everyday life-adapted and practical interior with the items, easy to clean, wash, relocate and demanding minimum costs and time to care about.